by Alexandra von Stauffenberg and Claudia Zeisberger*

Most family business founders aspire to build a firm that will last for generations to come. Sadly, that’s a rarity: According to Gallup, less than one-third of global family firms outlive the founder, and a scant 12 percent make it to the third generation.

Inadequate succession planning is often blamed for low rates of generational transfer. However, succession is only one facet of a much broader slate of policies and practices that promote longevity in family business. The term for this brand of business discipline is institutionalisation. Without it, family firms are defenceless against the threats to leadership, governance, talent management and decision-making that unavoidably crop up for all organisations that survive past the early developmental stages.

INSEAD’s Global Private Equity Initiative (GPEI) is in the midst of conducting a global research study into the institutionalisation journeys of family businesses in various regions of the world. In recent years, the GPEI has released reports on Latin America and Asia-Pacific and the Middle East. Applying the same framework, we have now broadened our focus to the no less diverse and challenging terrain of Europe. The resulting report, The Institutionalization of Family Firms – Europe, was drawn from in-depth survey data provided by 121 family firms as well as several leading private equity (PE) firms with experience investing in family business.

Six attributes of institutionalisation

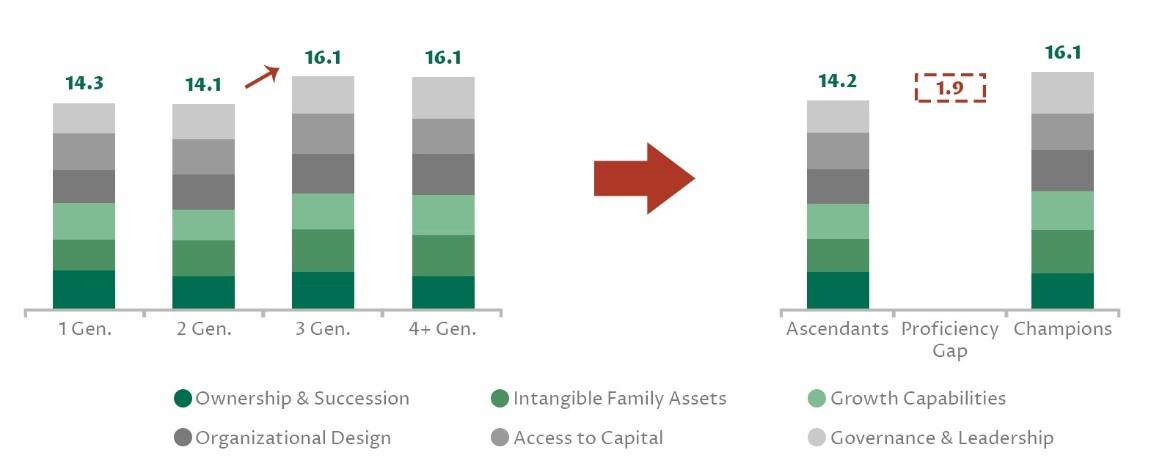

For all three reports, we defined institutionalisation according to six main attributes: family ownership and succession, intangible family assets, corporate governance and leadership, growth capabilities, organisational design, and access to capital. We also divided the participating firms into two groups based on longevity. Comparing the total institutionalisation scores across generations, we then identified the two generations between which the scores register the sharpest increase. We termed family firms in generations prior to this kind of proficiency gap as “Ascendants” and family firms in the generations that follow this gap as “Champions”.

Exhibit 1: level of institutionalisation by generation - Europe

Across the six attributes, Champions scored much higher than Ascendants (echoing similar results in the past two reports). But the proficiency gap could not be ascribed equally to all six. Intangible family assets – encompassing a family firm’s unique heritage, values and stakeholder networks – was responsible for 32 percent of the variance. The next largest contributors to the gap were corporate governance and leadership (30 percent) and organisational design (27 percent). The remaining attributes were less salient from a longevity perspective: growth capabilities accounted for only 14 percent, and access to capital was all but flat at 3 percent.

Surprisingly, Ascendants outscored Champions by 6 percent on family ownership and succession, largely because Champions had more family members who owned shares in the business, and had more family members who were employed or wished to be employed by the firm. Moreover, Champions reported more disagreements amongst the leadership on key operational issues, succession planning and shareholding structure. The conflict-resolution mechanisms in Ascendants were also slightly less well-developed than in Champions. This result underlines how important the attribute “Family Ownership & Succession” is along the institutionalisation journey.

Regional comparisons

As described above, in Europe, the difference in institutionalisation score was at its most pronounced between the second- and third-generation firms.

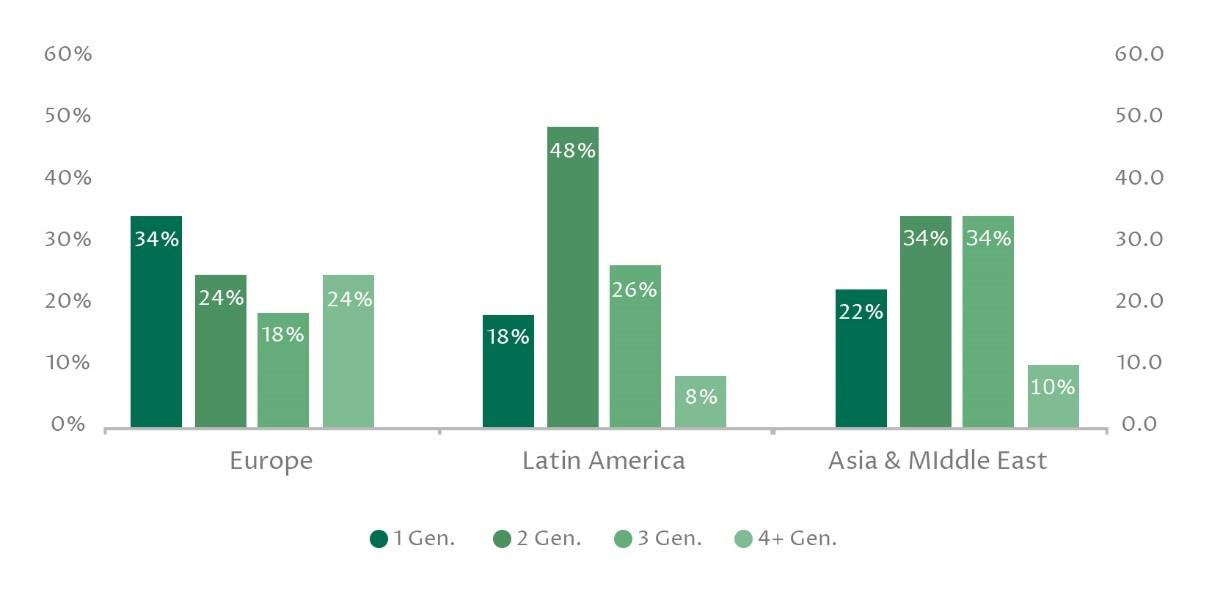

However, for Latin America and Asia-Pacific/Middle East, the gap did not appear until the fourth generation, suggesting that European family firms tend to institutionalise faster than their emerging-market counterparts.

Of the three regions, Europe featured the narrowest gap between Champions and Ascendants, less than half the size of the disparity in Asia-Pacific & Middle East. Yet first- and second-gen European family businesses start out with a slightly longer way to go, trailing behind peer firms in the other two regions. By the third generation, however, they have pulled ahead, again illustrating the greater speed of the institutionalisation journey in Europe.

Comparing our sample data across the three reports, Europe boasts a proportion (24 percent) of fourth-gen-and-beyond family firms that is more than double those of the other two regions.

Exhibit 2: survey participants by generation

Private equity

By providing capital and expertise, PE can serve as a vehicle for speeding up the institutionalisation of family firms. While family businesses usually operate to a multi-generational timeline, PE firms aim to effect transformation of portfolio companies over a relatively short period of time (generally within four to seven years). Nonetheless, in certain instances, PE firms and family businesses can form fruitful partnerships, particularly when family firms are in the process of institutionalisation or to enter the next phase of growth. Based on interviews with PE professionals experienced in investing in European family firms, the GPEI report explores the complexities and dynamics of these partnerships, describing the challenges and opportunities PE firms face at all three stages of the investment process (pre- and post-investment, as well as exit).

The most common reasons for family firms to partner with a PE firm are either company growth or some sort of family involvement. In the pre-investment phase, to build trust on both sides, PE firms must take the time to fully understand the family firm’s business vision, as well as their goals upon exit. Because they are more emotionally involved in their businesses, families seek a partner who will provide “the right home” for their business. They look beyond the highest bid to a range of factors including the quality and reputation of the PE investor, the strategic fit, the value a PE partner can bring to the table and potential governance changes. One interviewee likened the PE-family firm partnership to a marriage.

Post-investment, PE firms try to extract value from a family firm’s operations largely by eliminating inefficiencies. According to the interviewees, considerations in this phase are appointing an effective board, meeting talent shortages, managing family members in the business, strengthening systems and processes, M&A and internationalisation, maintaining strong stakeholder relationships and overcoming resistance to change. When done right, such institutionalisation measures can create long-term value.

However, the report also highlights some pitfalls that can arise during the partnership. For example, difficulties may arise because of a shift to a more meritocratic culture that demands high performance from relatives and non-relative alike. Moreover, occasionally, clashes can erupt between the new managers and long-term employees whose primary loyalties lie with the family. There is also the danger that due to the new ownership structure, certain intangible assets that provide unique advantages, such as the rich customer relationships that veteran employees have developed over time, may weaken drastically.

PE firms are usually careful to include clearly defined exit terms in every deal before it is signed. Even so, alignment must be regularly reinforced through verbal discussions with the family. As one interviewee said, “If both parties get to a stage where they are quoting legal terms to each other, you know you’re not in a great place.”

Another anecdotal finding in the report is that family firms are increasingly seeking to buy back equity they have sold. For these firms, the partnership with PE is a marriage of convenience designed to add value to the business. Once that mission is accomplished, the family moves to recapture full ownership.

*Associate Director at the INSEAD Global Private Equity Initiative and Senior Affiliate Professor of Decision Sciences and Entrepreneurship & Family Enterprise at INSEAD and the Academic Director of the school’s Global Private Equity Initiative

**first published in: knowledge.insead.edu

By: N. Peter Kramer

By: N. Peter Kramer