It is not just in Japan that shareholder power is not all it's cracked up to be. The owners of public companies the world over frequently find themselves powerless. In America, shareholders sometimes must contend with poison pills that stop them selling their shares to a bidder that the board dislikes, and even more often with rules that allow managers to decide which motions shareholders can vote on at their firm's annual meeting. In Europe, meanwhile, shareholders count themselves lucky if they even have a vote.

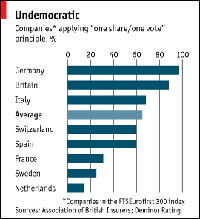

A new study prepared for the Association of British Insurers (ABI) by Deminor Rating, a Belgian governance consultancy, highlights the weakness of European shareholder democracy. As the chart shows, only two-thirds of the big European firms included in the FTSE Eurofirst 300 index operate a rule of one share, one vote. In the other third of firms, power tends to be concentrated in the hands of a minority of big shareholders who control a majority of the voting rights.

Practice varies widely across Europe. A mere 14% of the firms in the sample from the Netherlands allow their owners one vote per share; 25% of the Swedish firms; and 31% of the French companies. Things are far more democratic in Germany (97%) and Britain (88%). One-fifth of the companies issue shares with multiple voting rights, giving additional votes to selected shareholders. One in ten firms imposes a ceiling on the number of votes that can be exercised by any one shareholder, irrespective of how many shares he owns.

The ABI, which represents a group of big institutional shareholders, commissioned the study because of its frustration with the failure of the European Union's new takeover directive to require fair votes for shareholders. This failure, points out the ABI's Peter Montagnon, means that Europe is unlikely to develop soon the lively market for corporate control that it urgently needs.

By: N. Peter Kramer

By: N. Peter Kramer