by Estelle Xue Liu, Karim Foda and Sebastian Weber*

One of the positive surprises about last year’s recession is how little damage it inflicted on average household and corporate balance sheets in Europe.

In the past, deep recessions were followed by protracted weakness as they left households and businesses with significantly higher debt and lower income and capital. So far this has not been the case with the COVID-19 crisis, largely thanks to the extraordinary policy response by governments and central banks.

As the recovery takes hold, however, policy makers will need to maintain support for the hardest hit segments of the economy and remain alert for signs of economic damage yet to emerge. Not all private balance sheets were equally resilient.

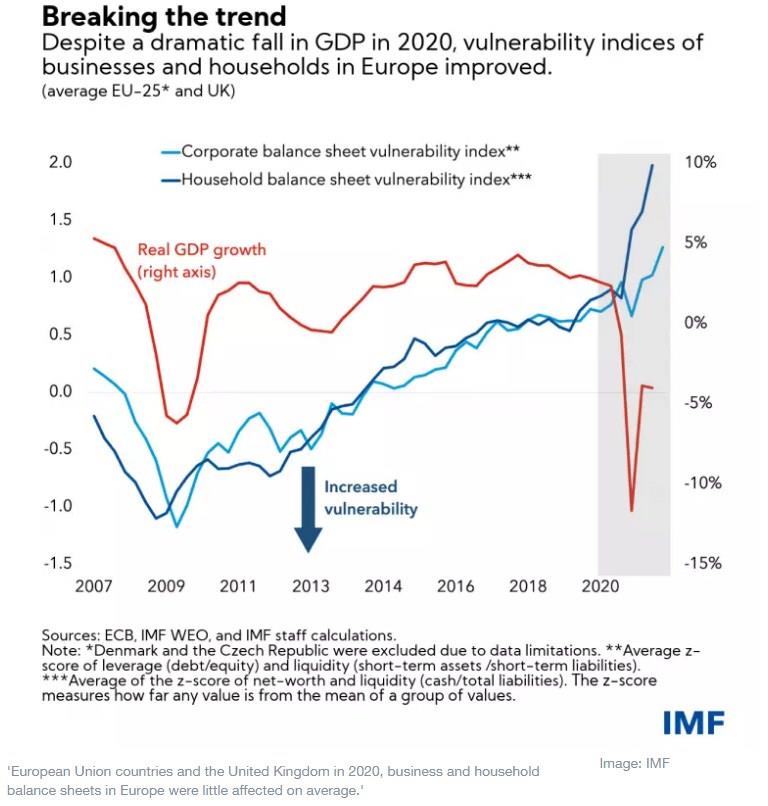

In new IMF staff research, we observe the resilience of private sector balance sheets. For example, using a simple balance sheet vulnerability index, which combines measures of leverage (or indebtedness) and liquidity, we can see that despite the collapse in GDP in European Union countries and the United Kingdom in 2020, business and household balance sheets in Europe were little affected on average.

Before the pandemic, these indicators tended to move in tandem – declining GDP was usually accompanied by increased strain on corporate and household balance sheets. In contrast, even in the worst phase of the crisis last year, the index for the corporate sector in Europe only fell marginally—and by the end of 2020 the index actually improved. Although these sector-wide observations mask the diverse range of outcomes at the industry or firm level, particularly among those hardest hit by the pandemic, they underscore the resilience of the corporate sector as a whole.

European household balance sheets also improved in aggregate in 2020, despite higher unemployment and shorter working hours. People stayed home more and spent less, while policy measures supported their income.

The support to businesses and households also reinforced financial stability because of the key roles they play as investors, borrowers, and depositors. Their resilience prevented a deterioration of the assets of European banks and other financial institutions.

Who bears the cost, and when?

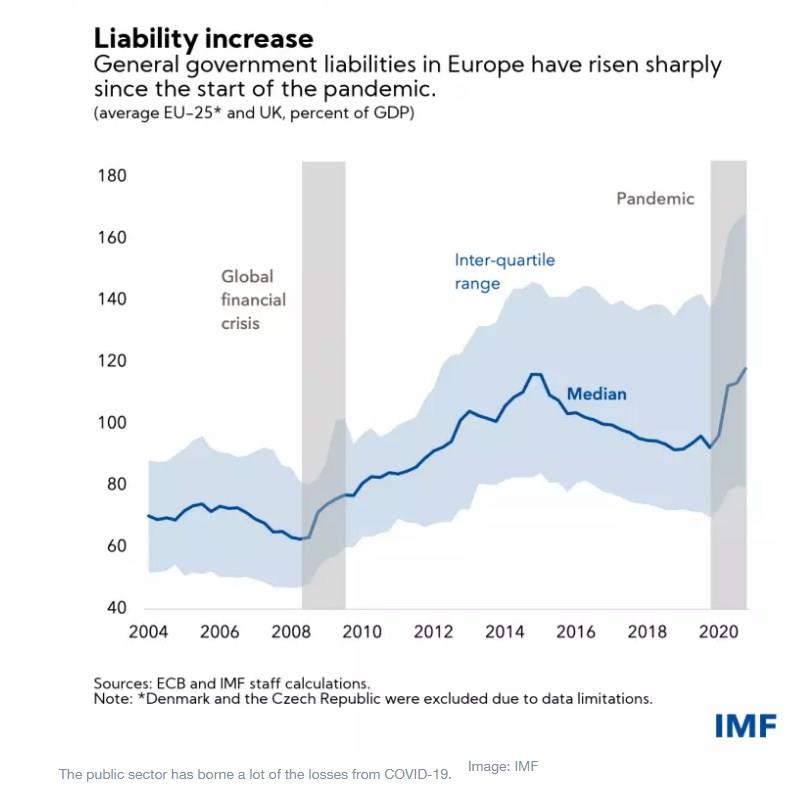

But if business and household balance sheets did not bear most of the losses from the COVID-19 crisis in Europe, then who did? The short answer is “the public sector.”

On top of traditional policy instruments such as unemployment insurance schemes, large emergency policy packages, including wage subsidies, grants, tax deferrals, and guaranteed loans, supported private-sector incomes and their financial strength. But they also increased government debt in 2020 (net of government deposits) by more than 5 percent of GDP in half of the countries and by more than 12 percent of GDP in seven others.

Central banks and private banks have purchased much of this new public debt. Asset purchase programs by central banks particularly helped maintain stable and low borrowing costs for government debt. Low interest rates also supported equity valuations while economic activity was depressed. Together with financial regulatory relief, such as loan repayment moratoriums and bank capital relief, these policies helped preserve equity and boost liquidity in the private sector, preventing a deterioration of business and household balance sheets.

The path ahead

Preventing the COVID-19 crisis from severely damaging private balance sheets is key to laying the foundations for a successful recovery in Europe. The extraordinary policy response to date has been the right thing to do in the face of an unprecedented exogenous shock.

But the pandemic is not over, so these gains need to be maintained in the next phase of the recovery. Risks to economic activity remain, including to private sector balance sheets if the pandemic is not fully controlled, thus warranting continued policy support for now.

The path ahead presents a delicate balancing act. As vaccinations advance and the economic recovery gathers steam, broad emergency support should give way to policy interventions increasingly targeted at the worst hit household groups and firms.

Recent studies indicate that there are pockets of acute vulnerability within certain industries and household groups, even if the aggregate picture for both sectors offers comfort. Thus, addressing solvency needs of viable firms in hospitality and other contact-intensive services, as well as providing further assistance to the self-employed and vulnerable households remains essential. But public balance sheets are not without limits and so the policy debate will turn to the appropriate path of reducing public sector indebtedness in due course.

After COVID-19 is under control and the recovery is firmly underway, uncertainty will diminish and it will be possible to roll back emergency support measures. This process may present challenges of its own, as some hidden economic damage may only become visible then. Managing these hidden risks calls for a gradual and cautious approach.

*Senior economist in the European Department , IMF and Economist, European Department of the IMF and Senior Economist in the European Department, IMF

**first published in: www.weforum.org

By: N. Peter Kramer

By: N. Peter Kramer